The New Economics of Retrofit in Social Housing

- Eleanor Bowden

- Mar 10

- 2 min read

Updated: Mar 31

The Regulator of Social Housing’s Sector Risk Profile is rarely described as a page-turner, but the latest edition contains a figure that should make every housing association boardroom sit up.

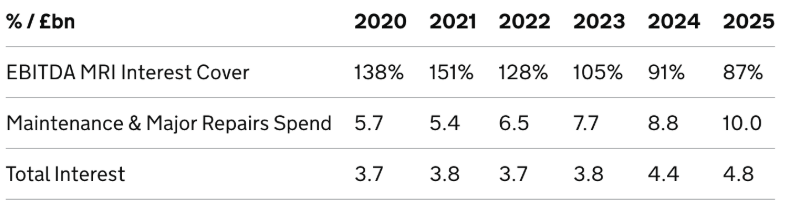

For the first time since the financial crisis in 2008, interest cover (EBITDA MRI) has fallen to 87%.

In other words, the sector is currently spending more on interest and maintenance than it is bringing in. The financial cushion that historically allowed housing associations to absorb shocks has, for the moment, reached its limit.

This would be a challenging enough backdrop on its own. The Government’s New Decent Homes Statement, alongside its Warm Homes Plan announced earlier this year, introduces a new 2039 target for Minimum Energy Efficiency Standards. Meeting those standards will place further pressure on already stretched balance sheets.

The Funding Gap

On one hand, the Regulator is highlighting that balance sheets are at a fifteen-year breaking point. On the other, the Government is increasing the energy efficiency standards Registered Providers must meet. This is alongside the breadth of broader regulatory standards that are increasing to meet improved customer and asset standards.

The Regulator cannot insist that retrofit requirements be fully costed into 30-year plans because they recognise - and have publicly discussed - that doing so would compromise the sector's viability. The central problem is that the traditional funding model for retrofit, using capital expenditure backed by social housing debt, is hitting a ceiling. When interest cover is at 87%, the capacity to do the work and self-fund is no longer there.

A Shift in the Financial Model

At Pineapple Homes, we look at the emerging models that finance retrofit differently. We are seeing a necessary transition from a Capex cost to a variety of alternatives: off-balance sheet structures, OpEx-based models, and income streams from renewable energy are all emerging options.

We are currently seeing this play out in practice through our work with a group of housing associations in the North West. While still in the early stages, we are helping these providers explore potential new methods of funding retrofit and consider where collaborative action may be more commercially viable than individual delivery.

How to Navigate this Brave New World

Navigating this is complicated, and there are no off-the-shelf answers that work for every provider. It depends on your risk profile, your asset profile, and your relationship with your customers. We are currently working with a number of clients individually and in groups reviewing how these alternative approaches can function in a way that serves your customers, your balance sheet and your board.

If you are currently reviewing your 30-year plan and find that the inclusion of regulatory retrofit standards is turning the outlook more red than green, we’re always happy to share what we’re learning. If you’d like an informal, off-the-record chat about how these emerging models might fit your specific stock, do let us know. We can bring the data, and perhaps some better news than the latest Risk Profile.

Eleanor Bowden

Managing Director of Pineapple Homes